The Australian Dollar (AUD) steadied on Wednesday, erasing earlier losses as prospects for a Federal Reserve rate cut in September improved sentiment, while weakening bets of a Reserve Bank of Australia (RBA) rate cut added to support. Yet, the currency came under pressure following China’s August Consumer Price Index (CPI) decline of 0.4% year-on-year, which reflected lingering economic softness in Australia’s biggest trade partner. Better domestic data, such as a larger trade surplus, improved Q2 GDP growth, and hotter July inflation, have served to contain risks to the downside for the AUD. Market attention turns to the forthcoming US inflation data, which may offer clearer signals for the Fed’s policy direction.

KEY LOOKOUTS

• Over 93% chances of September 25 bps cut priced in by markets can weigh on the US Dollar and lift the AUD.

• 0.4% YoY drop in August CPI is a sign of weak demand in China, which may put pressure on the Australian Dollar because of trade relationships.

• Huge trade surplus, GDP expansion, and hotter inflation diminish prospects of imminent RBA rate cuts, providing AUD with some grounding.

• This week’s US PPI and CPI reports will be important in gauging the direction of Fed policy and AUD/USD action.

The Australian Dollar fluctuated with strength on Wednesday, aided by increasing expectations of a September Federal Reserve rate reduction and diminishing prospects of near-term easing by the Reserve Bank of Australia. Sturdy domestic underpinnings in the form of a bigger trade surplus, stronger-than-expected Q2 GDP growth, and increased July inflation countered the negative pressure from subdued Chinese inflation data that declined more than anticipated and reflects continued economic weakness in Australia’s main trading partner. As markets placed more than 93% probability of a Fed cut this month, the focus now shifts to future US inflation releases, which may steer the next big move in the AUD/USD pair.

The Australian Dollar remained stable as bets on Fed rate cuts improved sentiment, with top-tier Australian data capping downside risks. Weak Chinese inflation, however, kept the currency under pressure, with the focus now shifting to pivotal US inflation reports for direction.

• The Australian Dollar stabilized as anticipation for a September Federal Reserve rate reduction grew stronger.

• RBA rate cut expectations have eased on the back of Australia’s firmer trade surplus, GDP expansion, and hotter July inflation.

• China’s CPI dropped 0.4% YoY in August, pointing to continued weakness in Australia’s major trading partner’s economy.

• Markets now place in excess of 93% probability of a Fed 25 bps reduction this month, from 86% last week.

• US Nonfarm Payrolls increased a meager 22,000 in August, well short of projections, while unemployment ticked higher to 4.3%.

• Australian consumer confidence has deteriorated, portending possible requirement for future RBA easing despite short-term stability.

• Market attention turns to the coming US PPI and CPI releases, which will be instrumental for setting Fed policy expectations and AUD/USD direction.

The Australian Dollar gained some stability during the middle of the week as markets factored in firmer chances of a September Federal Reserve interest rate cut, and dovish expectations on short-term Reserve Bank of Australia (RBA) action provided further support. The economic environment for Australia is still quite solid, with a larger July trade surplus, better-than-forecast second-quarter GDP growth, and hotter-than-expected July inflation supporting the case for the RBA to keep policy unchanged in the near term. All these have assisted in protecting the AUD from external pressures, especially from China’s softer economic performance.

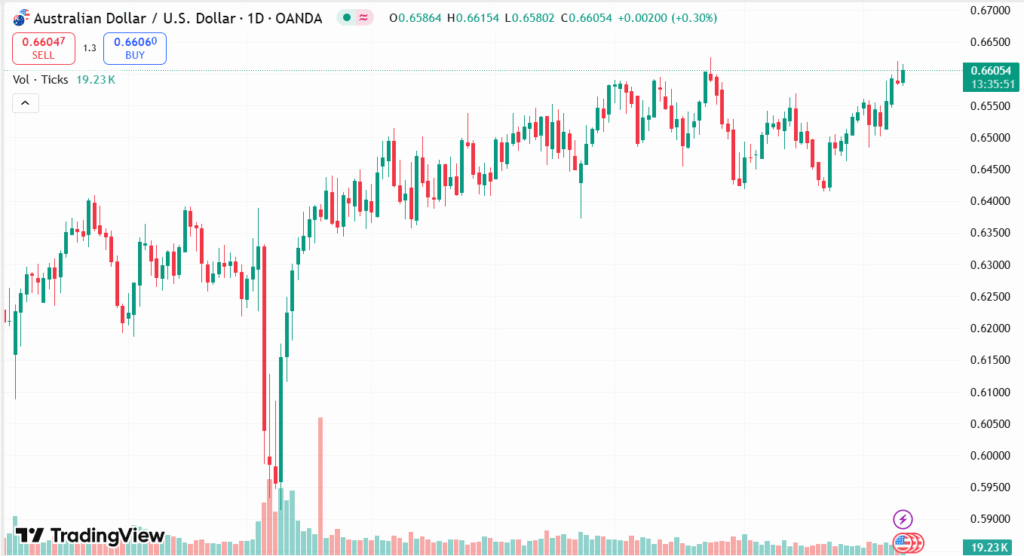

AUD/USD DAILY CHART PRICE

SOURCE: TradingView

China’s Consumer Price Index (CPI) fell by 0.4% year-on-year in August, highlighting weak demand in the world’s second-largest economy and Australia’s most important trading partner. This puts in doubt how weakness in China can spill into Australian exports. While in the United States, the labor market is softer than earlier anticipated, with Nonfarm Payrolls falling below forecast and benchmark revisions indicating weaker employment growth. Market players now await US inflation reports, which will probably determine the next move by the Federal Reserve and affect overall currency market sentiment.

TECHNICAL ANALYSIS

The AUD/USD currency pair trades around 0.6580, showing a bullish inclination within its daily chart rising channel. The price stays above the nine-day Exponential Moving Average (EMA) of 0.6556, which indicates short-term buying momentum. The immediate resistance is the 10-month high of 0.6625 in late July, followed by the top of the rising channel at around 0.6640. A break above this range could provide the catalyst for a move towards the 11-month high of 0.6687. Conversely, a breakdown below the 0.6550–0.6556 area would undermine the bullish thesis, with the 50-day EMA level of 0.6512 being the next main support.

FORECAST

The Australian Dollar may get additional traction if future US inflation reports support the September Federal Reserve rate cut expectations. A dovish Fed perspective, combined with Australia’s stronger trade surplus, Q2 GDP growth, and higher July inflation, may aid further strength in the AUD/USD pair. A continuation above the 0.6625–0.6640 resistance area will most likely persuade buyers to move towards the 11-month high of 0.6687.

On the other hand, poor Chinese economic figures keep bearing down on sentiment, and any additional weakness in demand may cap the Australian Dollar’s upside. Unless the AUD/USD pair manages to stay above the 0.6550 support zone, it may move down towards the 50-day EMA level of 0.6512, with even deeper losses revealing the three-month low of 0.6414. Also, better-than-anticipated US inflation readings will postpone Fed easing intentions, providing the US Dollar renewed vigor and pushing the pair lower.